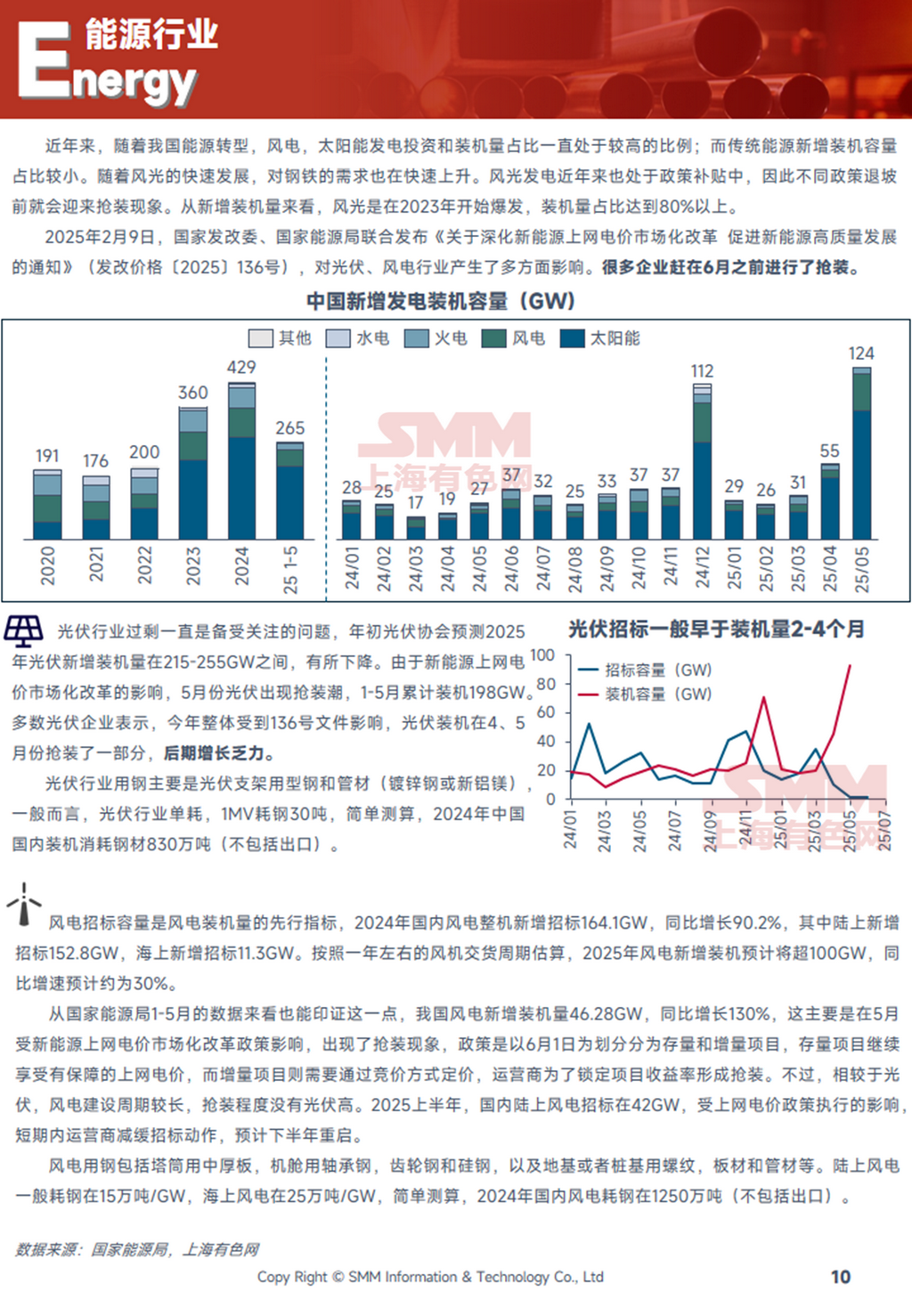

In recent years, with China's energy transition, investments and installations in wind and solar power have consistently accounted for a high proportion, while new installations of traditional energy sources remained relatively small. The rapid development of wind and solar power has also driven a surge in steel demand. Wind and solar power generation has been under policy subsidies in recent years, leading to installation rushes before subsidy phase-outs. From the perspective of new installations, wind and solar power experienced a surge starting in 2023, accounting for over 80% of total installations.

On February 9, 2025, the National Development and Reform Commission (NDRC) and the National Energy Administration jointly issued the "Notice on Deepening the Market-Oriented Reform of On-Grid Tariffs for New Energy to Promote High-Quality Development of New Energy" (NDRC Price [2025] No. 136), which had multifaceted impacts on the PV and wind power industries.Many companies rushed to complete installations before June.

According to SMM estimates, China's domestic PV installations consumed 8.3 million mt of steel in 2024, while the wind power industry consumed 12.5 million mt. From January to May 2025, domestic PV installations consumed 5.93 million mt of steel, up 150% YoY. Considering the significant reduction in installation rushes after June, steel demand for PV is expected to weaken in H2. For wind power, new installations in 2025 are projected to exceed 100GW, with a YoY growth rate of around 30%. Under the installation rush from January to May, growth already reached 134%, and wind power installations are also expected to slow down in H2.

The following content is excerpted from SMM's downstream operating rate report:

*This report is an original and/or compiled work created by SMM Information & Technology Co., Ltd. (hereinafter referred to as "SMM"). SMM legally owns the copyright and is protected by the Copyright Law of the People's Republic of China and other applicable laws, regulations, and international treaties. Without written permission, it is prohibited to reproduce, modify, sell, transfer, display, translate, compile, disseminate, or disclose the content to third parties in any other form or authorize third parties to use it. Otherwise, SMM will pursue legal actions against infringement, including but not limited to claims for contractual liability, restitution of unjust enrichment, and compensation for direct and indirect economic losses.

The content of this report, including but not limited to information, articles, data, charts, images, sounds, videos, logos, advertisements, trademarks, trade names, domain names, and layout designs, is protected by the Copyright Law of the People's Republic of China, the Trademark Law of the People's Republic of China, the Anti-Unfair Competition Law of the People's Republic of China, and other applicable laws and international treaties regarding copyright, trademark rights, domain name rights, commercial data information rights, and other legal rights. It is owned or held by SMM and its relevant rights holders. Without written permission, any organization or individual is prohibited from reproducing, modifying, using, selling, transferring, displaying, translating, compiling, disseminating, or disclosing the content to third parties in any other form or authorizing third parties to use it. Otherwise, SMM will pursue legal actions against infringement, including but not limited to claims for contractual liability, restitution of unjust enrichment, and compensation for direct and indirect economic losses.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)